What's Going On #1

What's Going On #1

The Fed, Commodities, Housing, Equities, and Crypto

Disclaimer: The views expressed represent Giancarlo Lamourtte’s opinions. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment.

All Eyes on Fed

Portfolios are bleeding and the stock market typically anticipates the economy. Markets move to price in future expectations, then we feel the results at home. This current moment is influenced by two factors, excess spending, and broken supply chains.

Remember the stimi check era? Good times…

A rush of short-term wealth followed. We were given “free” money while hunkering down and spending less. Supply chains halted, but as we came out of the pandemic, there was a rush in consumer demand as people wanted to spend their new wealth. Suppliers coming out from the lull of the pandemic couldn’t keep up with demand, causing shortages and price hikes. Now we’re paying for the sins of excess consumption. This spike in consumer demand is what the Federal Reserve is trying to stomp using two main tools: open market operations and the federal funds rate.

Open market operations allow the Fed to purchase securities on the open market, generally U.S. government bonds from banks. This floods the system with cash and allows banks to lend more money at a cheaper rate. The Fed has accumulated a large balance sheet of treasuries and other bonds over the last 15 years. Once the Fed stops purchasing and allows the bonds to mature, banks will have to reduce their cash positions and charge a higher interest rate on loans to businesses and consumers. This is called, “tapering” the balance sheet and is what the Fed intends to do during this quantitative tightening (“QT”) cycle.

The federal funds rate is the rate at which commercial banks can lend to each other, and is controlled indirectly by the Feds’ open market operations and how they set the discount rate. The discount rate is the rate at which commercial banks can borrow from the Federal Reserve. Everyone debates how high or low the Fed should set the federal funds rate because it acts as the baseline interest rate for all consumer loans.

The following chart shows the relationship between CPI—the measurement of inflation—and the federal funds rate:

The two generally move in lockstep because the federal funds rate is the Fed’s primary weapon against inflation, but there has been a major spike in the disparity between the two over the past 2 years. There are two likely reasons: The Fed dragging its heels on raising rates and Russia’s invasion of Ukraine dramatically changing global trade.

The Eastern and Western hemispheres have always been divided. We can go as far back as 499 BC and learn about the wars between Ancient Greece and Persia. Even before recorded history, this attitude towards the “other” has always been an aspect of human nature. Presently, this global conflict of East vs. West shines on the United States and China and has escalated year over year—coinciding with China’s meteoric rise over the last 20 years. However, we’ve reached a tipping point and entered a new world order brought to us by Russia’s invasion of Ukraine. We’re now faced with economic battles between nations cutting each other off from necessary resources, and supply chains have once again been fractured. Unlike the pandemic, this issue can persist for much longer and our economy needs time to adjust to the new paradigm. This supply shock has worsened the inflation issue and is something that cannot be fixed by the Fed raising rates, giving time for the economy to adjust seems like the only antidote.

Chess… but with Commodities

For many years the world, especially the United States, has benefited from friendly relations and free trade. We became the global consumer but recent events have put a halt to our WALL-E future.

The war in Ukraine has sprung a new era where nations are playing economic chess and hoarding their natural resources. Now, the commodities market is more important than ever. Behind each movement in the price of grain, oil, etc., there’s a critical geopolitical story.

Oil is all the rage these days. No matter how badly we’d like to cut this resource from powering our Pelotons and espresso machines, to quote Kyla Scanlon, “You cannot have green energy policy without green energy investment.” Nations have succeeded in promoting the allure of climate consciousness, but have failed at making the proper investments to remove their dependence on oil, especially the Russian type. This has been the biggest hit to European nations.

The EU has put together a proposal to inject 210 million euros of total investment to eliminate Russian fossil fuels by 2027. Most EU states would have to implement the embargo within the first few months, however, Hungary stopped the proposal from obtaining the required unanimous approval from all 27 member countries. Hungary is heavily dependent on Russian oil and has said they would need 750 million euros in short-term investments to withstand the embargo.

We’ve also seen a record number of Russian oil cargo ships at sea. Most of this oil will go to China and India, but volumes to Europe have increased. The price of oil has soared as nations are clamoring to buy more before implementing a ban on Russia. Others need to shore up energy security as they have already depleted oil reserves attempting to fight rising prices.

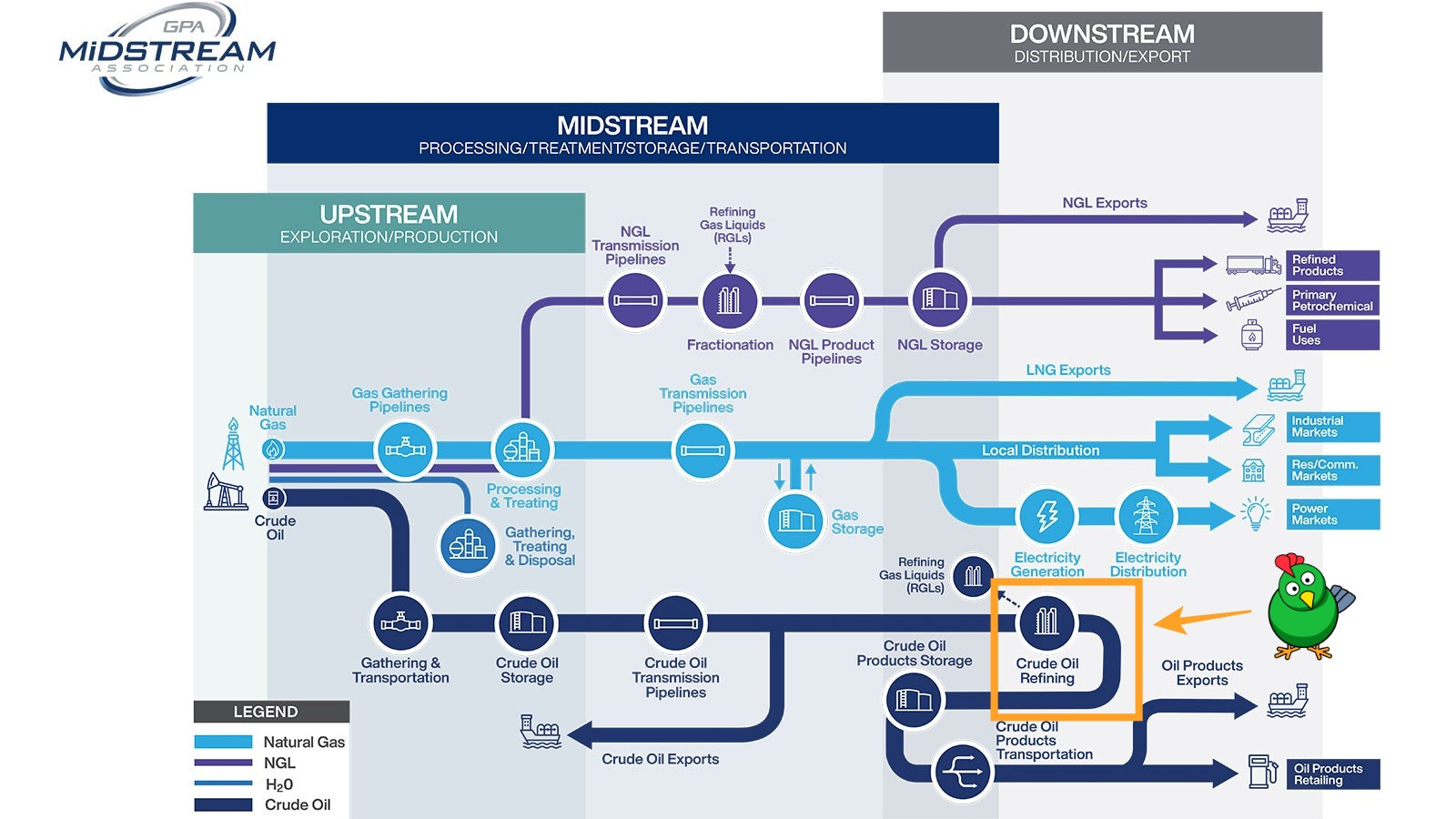

It’s hard to understand how this has happened given the obvious importance of energy, but we must understand how intricate and fragile this supply chain is. See the following diagram that helps visualize the process:

Oil and gas pass through hundreds of hands before reaching the pump and power plants. It’s a complex process that will take time to repair.

Wheat has also faced critical constraints as of late. Russia and Ukraine account for nearly one-third of the world’s wheat supply which has already increased the global price for wheat. Last Friday, India—the second-largest wheat producer—banned exports of the grain in an attempt to fight rising food prices. This was following one of the hottest months on record for India, which led to many damaged crops. These shortages are already taking shape in the real world. Somalia faces one of the worst droughts and food shortages in decades and roughly 6 million Somalis will need aid to survive. With all eyes on Ukraine, it seems unlikely they will receive sufficient help.

We also have the lumber market which has been a roller coaster. Here’s lumber’s wild ride over the past year:

The price has fallen as far as -72%, risen back over 200%, only to fall back -54% to its current price. If you know anyone who’s been building or renovating their home within the past couple of years, then you’ve heard the ordeal over raw materials. My brother—who’s been renovating his house for the last 9 months—has personally given me a collegiate-level lecture on the shortage of raw materials, and one of the key components of a home is lumber. See the price of lumber since 2004:

These volatile movements have been a phenomenon of the pandemic supply clog. Prices have leveled out over the past few days and we hope to see this trend continue. This may be perfect timing as we’re seeing the first signs of the end of the housing shortage.

So You’re Saying I Can Own Property?

Someday, maybe! The past few years have seen a huge shortage in the supply of homes for many reasons listed above, i.e., 15 years of low-interest rates and 2 years of raw material shortages. Those trends are now being reversed. The Fed is finally raising interest rates and mortgage rates are rising at an even faster pace. Housing inventory is up 43% since the beginning of March 2022 and up 8.2% week over week. So we’re seeing some relief, and the supply and demand trends for housing have reversed. Hopefully, we can find some normal equilibrium as 19% of US home sellers have dropped their prices to find new buyers.

Finding this new price equilibrium will result in real estate prices contradicting a bit, and we may see this over the next few weeks or months. It’s only fitting since all assets are being crushed. Real estate tends to lag broader markets as it takes property owners time to factor in all these changes.

The End of Stonks

Back to our bleeding portfolios… The Fed’s stimulus—mixed with our excess buying of all assets during 2020—has led to where we are. Where we go from here is an entirely different question.

Greg Jensen, Co-Chief Investment Officer of Bridgewater Associates, recently went on the Odd Lots podcast to discuss his outlook on the market. Bridgewater is known for compiling massive amounts of data, running it through algorithmic models, and using artificial intelligence to help predict future outcomes. One piece of the analysis showed:

40% of the US equity market can’t sustain valuations without new investor inflows. This data point is key to understanding the recent movement of the market, and where we may go. The market is basically pricing in, less liquidity from Fed = market go down. There’s also been a trend over the past few years where the market has consolidated around a few big tech companies. These tech stocks have been the main contributor to the past bull run and our recent downturn.

“Live by the sword, die by the sword.”

Many try to compare this market to those of the past. Whether it’s the cycle of the 70s, early 2000s, or 2008, the reality is each cycle is different. This current one is complex, but there’s light at the end. The retail investor has hitched a ride out, and this usually indicates a bottom. Unfortunately, we retail normies tend to get it wrong most of the time, and when retail leaves it’s time for institutional capital to come in and play.

There’s always hope in data, and history shows the market will come back. Patience is a virtue and you will be rewarded. This is the importance of making decisions using a long-term framework.

Crypto: New Beginning

If equity markets don’t satisfy your risk appetite, then crypto is just your speed! $BTC and $ETH are down around 50-60% while other tokens have fallen roughly 70-90%. Public markets have taken a beating. Luckily, price action doesn’t waver the urge for developers to continue building products. Crypto companies will continue to grow, and private markets are reaping the rewards. StarkWare closed a funding round this week putting them at an $8 billion valuation, along with Andreesen Horowitz raising a new $4.5 billion crypto fund. Investment in the space will slow with growing macro concerns, but no other space has been attracting young talent quite like the crypto industry. Time favors those who are patient.